US - Iran Escalation

Navigating Uncertainty with Portfolio Resilience

• Geopolitical risk has escalated sharply, with coordinated US‑Israel strikes on Iran marking a rapid shift to military action and reinforcing the relevance of geopolitical shocks for investment strategy

• Market reactions have followed historical patterns, with oil and gas prices rising on supply and transit concerns, while equity markets have softened most notably for energy importer regions

• Our scenario‑based framework remains central, balancing long‑term return objectives with portfolio positioning designed to manage volatility, supported by high‑quality equities, government bonds, liquidity, US‑dollar assets and gold

• The key uncertainty is the path of military escalation and energy disruption, particularly Iran’s ability to impair oil and gas flows through the Strait of Hormuz, with implications for inflation and growth

• Our constructive and diversified portfolio stance remains intact, but the balance of risks around inflation and growth has shifted higher, requiring continued vigilance and flexibility as events evolve

Events over the weekend are a stark reminder of how quickly geopolitical tensions can move from rhetoric to military action, and of the material implications this can carry for investment strategy. In our 2026 Annual Investment Outlook we highlighted the underappreciated risk of escalation, noting that “regime change in Venezuela could foreshadow a broader willingness by the US administration to intervene elsewhere in Latin America or the Middle East.”

That risk has now crystallised. Coordinated US-Israel strikes on Iranian targets included the killing of Supreme Leader Ayatollah Ali Khamenei and dozens of senior political and military figures, prompting a swift Iranian response directed at Israel and at US military installations across the Gulf.

Initial market moves have been broadly consistent with historical precedent. Oil prices have risen sharply, reflecting Iran’s influence over global supply and critical transit routes, while global equity markets have retreated as investors adopt a risk-averse stance.

Investment Strategy: Scenario Analysis in Action

Our approach is anchored in the long-term preservation and growth of real wealth, informed by scenario analysis across policy, geopolitics and key investment themes. Whilst strategic allocations to equities and credit are guided by long run return potential, portfolio positioning at any point in time reflects our assessment of the risk of abrupt shocks or regime shifts with adverse market consequences. In that context, exposure to high quality, resilient businesses, alongside physical gold, government bonds, money markets and US dollar assets, remains central to sustaining portfolio resilience.

In recent months we have maintained a constructive view on global risk assets, supported by the prospect of policy tailwinds and a gradual rotation within markets, underpinning earnings and returns over time. The escalation in military activity, however, raises a legitimate question: do our working assumptions for growth, inflation and, ultimately, portfolio strategy require reassessment?

Military Escalation: What Comes Next?

Whilst the risk of a prolonged conflict is front of mind, our current assessment remains that President Trump is pursuing a swift, decisive campaign aimed at materially degrading Iran’s military capabilities, whilst creating the conditions for a face-saving negotiated outcome with the remaining leadership. The economic and political costs of a broader objective, such as outright regime change, are likely to act as a constraint in this midterm year, notwithstanding the administration’s confidence following its perceived success in Venezuela. Accordingly, the willingness of Iran’s remaining leadership to engage in dialogue and deescalate, to preserve the regime, has become a critical variable for markets.

To date, Iranian retaliation via ballistic missile strikes appears to have been widely intercepted, and the regime has already been significantly weakened. The economic pressure resulting from the US-Israel operation may ultimately prove intolerable. Nevertheless, Iran retains meaningful leverage through its capacity to disrupt global energy markets. The Strait of Hormuz is a critical chokepoint for oil and gas flows; sustained impairment would have further implications for energy prices, inflation expectations and broader financial conditions. As of Tuesday 03 March, reports suggest traffic through the Strait is running at less than 20% of normal levels, with drone activity and GPS interference deterring commercial shipping. Disruption to Qatari Natural Gas infrastructure has also been significant following reported Iranian drone strikes, sharply reducing production.

Current market pricing appears to assume the disruption will be temporary, with the recent move in energy prices reflecting a near term ‘worst case’ premium. However, a more prolonged or disorderly destabilisation of Iran could see competing factions attempt to restrict passage through the Strait for an extended period, increasing the likelihood that the US and other major producers would need to draw on strategic inventories to stabilise markets.

Economic Impact: What Matters Most?

At this juncture, two variables matter most, and are inherently difficult to forecast: how long Iran can withstand the economic pressure imposed by the US-Israel strikes, and how effectively it can disrupt oil and gas supply chains.

Assuming a short, successful operation from the US perspective, that limits further oil and gas price spikes beyond what has already occurred, the macroeconomic impact should be contained. At current levels of $75–80, oil benchmarks remain within the trading range of the past three years. For the US, as a net exporter of oil, the threshold for severe economic damage is higher, with modest implications for inflation expectations. Prior economic and market momentum should be gradually restored by broad policy tailwinds and robust corporate earnings growth.

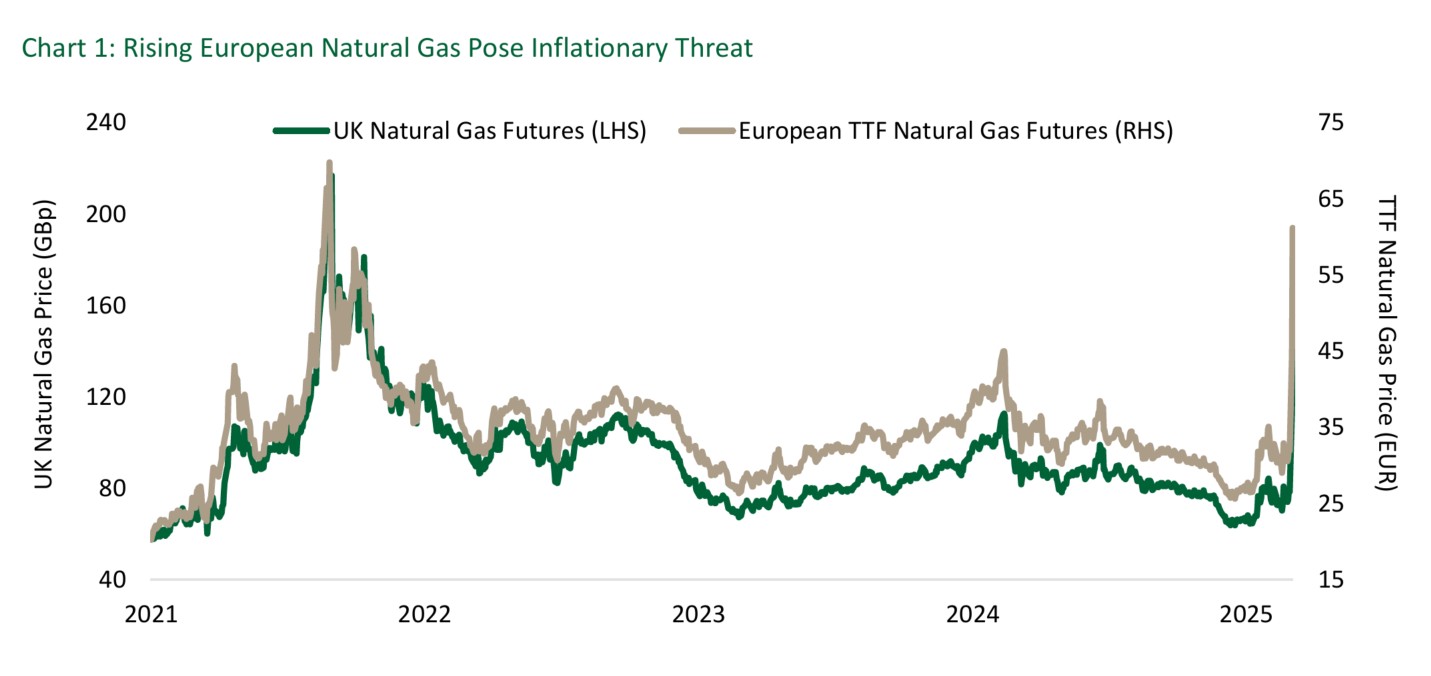

European and Asian economies, by contrast, are more exposed due to their greater reliance on imported energy. Natural gas prices have risen sharply (Chart 1), approaching comparable levels to the 2022 peak following the Russian invasion of Ukraine. In this case the outlook is more balanced, with a requirement to pivot energy supply and minimise disruption, avoiding a derailment of the growth recovery witnessed over the past 12–18 months.

Summary

Periods of heightened uncertainty underscore the importance of remaining anchored to long‑term investment

principles. The scenario framework underpinning our constructive and resilient strategy remains intact, whilst the risk of a more pronounced escalation, that could impair medium‑term return prospects, requires continued adaptability and flexibility in portfolio positioning. Core exposure to US markets has helped cushion near‑term volatility, complemented by the diversification benefits provided by physical gold, catastrophe bonds and risk‑managed alternative strategies. We continue to monitor developments closely, assess their broader implications for portfolio strategy, and will communicate further as conditions evolve.

RISK DISCLOSURE :

This document has been prepared for information only and to be used with existing clients only. It is not intended for onward distribution. It is neither an offer to sell, nor a solicitation to buy, any investments or services.

The information on this document does not constitute legal, tax, or investment advice. It does not constitute a personal recommendation and does not consider the individual financial circumstances, needs or objectives of the recipients. You must not, therefore, rely on the content of this document when making any investment decisions.

Whilst every effort is made to ensure that the information provided to clients is accurate and up to date, some of the information may be rendered inaccurate by changes in applicable laws and regulations

Issued by Stonehage Fleming Investment Management Limited (SFIM). Authorised and regulated by the Financial Conduct Authority (FRN.194382) and registered with the Financial Sector Conduct Authority (South Africa) as a Financial Services Provider (FSP No. 46194).